Flexi Cap Fund vs. Multi Cap Fund: Which One is Right for You?

Let’s be honest, if you’ve ever tried to pick the “right” mutual fund, you probably ended up staring at your screen, wondering what half the terms even meant. “Flexi Cap? Multi Cap? Aren’t they kinda the same?” Yeah, I’ve been there too. They sound similar. They both spread your money across large, mid, and small companies. So what’s the big deal?

Well, it turns out, the devil’s in the details. And when it comes to investing your hard-earned money, those details matter a lot.

This article isn’t about throwing jargon at you. It’s about helping you figure out what suits you. Not the investor in the next cubicle or some finance guru on YouTube. Just you, your goals, and your appetite for a little or a lot of market drama.

First Things First: What Are These Funds Anyway

Okay, let’s start with the basics — stripped down, no fluff.

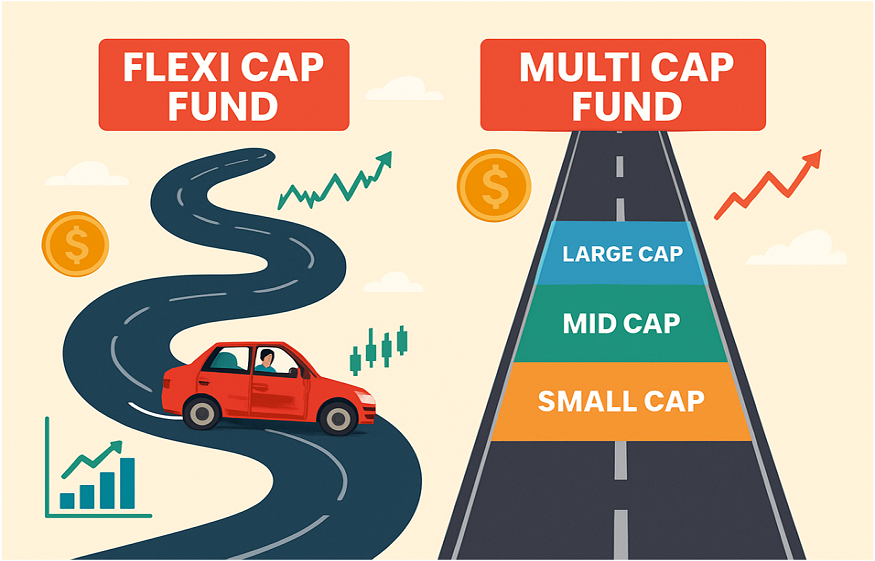

A Flexi Cap Fund is like a shapeshifter. It doesn’t have to follow any strict rules about how much money goes where. The fund manager can move your investment around — from large-cap to mid-cap to small-cap stocks — whenever they feel it’s time for a change.

On the other hand, a Multi Cap Fund has a bit more structure. By regulation, it must invest at least 25% of the portfolio into each of the three — large-cap, mid-cap, and small-cap stocks. So it’s got a built-in balance, but less wiggle room.

Sounds simple? It is, kind of. But the implications — oh boy — they go way deeper.

What’s Really Going On Behind the Scenes?

Imagine you’re building a cricket team. With a Flexi Cap, the coach (your fund manager) can pick anyone based on form – more experienced players if the pitch is tough, or younger, energetic guys if the match calls for it. They can shift the strategy mid-game.

A Multi Cap Fund coach, though, has a rulebook. You must have 25% seniors, 25% freshers, 25% all-rounders… no matter how the match is going.

That flexibility in Flexi Cap Funds can be a blessing or a curse. If your fund manager is sharp and reacts well to market signals, great. But if they mess up their judgment? Well, you’re riding shotgun on a rollercoaster you didn’t sign up for.

Let’s Talk Real-Life Scenarios

Picture this. The market’s going crazy. Small-cap stocks are tumbling left, right, and center. Now, a Flexi Cap Fund manager can take the wheel, shift gears, and pull out of small caps. They might go heavier on large-caps, the safer bets.

But a Multi Cap Fund? Nope. It has to stick with at least 25% in small-caps, even if those are crashing like a house of cards. That’s the rule. Hands tied.

So, when times are tough and let’s face it, they do come Flexi Caps can be a bit more defensive. But in good times? That mandatory small and mid-cap exposure in Multi Caps can shine.

A Word on Risk – Because It Matters

Let’s not sugarcoat it. Investing is risky. Full stop.

But not all funds carry the same kind of risk. Multi Cap Funds, because of their compulsory small-cap exposure, tend to be more volatile. You might see jaw-dropping gains one year and frustrating dips the next.

Flexi Cap Funds, depending on the manager’s calls, might smooth out that ride. They can lean conservative when needed and aggressive when the timing feels right.

But that’s the catch- you’re relying a lot more on the manager’s skill. It’s kind of like giving someone the keys to your car and saying, “Drive me safely to wealth.” Great, if they’re a pro. Not so much if they’re just guessing.

Okay, But What About Returns?

Ah yes, the million-rupee question. Which one gives better returns?

And the honest answer? It depends.

If the markets are in a sweet spot, the economy’s growing, small businesses are booming — Multi Cap Funds can deliver stunning results. That mandatory 25% in small-caps can supercharge your portfolio.

But if there’s a downturn? Or a crisis? Those same small-cap companies could nosedive, dragging your returns with them.

Flexi Cap Funds, being more nimble, can avoid some of that damage. They may not always outperform in bull runs, but they often protect better in bear markets. It’s a classic case of offense vs. defense.

So, Who Should Invest in What?

This is where things get personal. Not emotional, but personal.

If you’re someone who:

- Is just starting out with mutual funds

- Doesn’t want to think too hard about “what’s the market doing today?”

- Would prefer a fund manager to handle the heavy lifting

Then Flexi Cap might be a great match.

But if you’re a bit more seasoned or simply willing to stomach more volatility and you believe in the long game (I’m talking 7–10 years), Multi Cap Funds might reward your patience. Especially if you’re okay with the fact that some years might be a bumpy ride.

Honestly? There’s no one-size-fits-all here. It comes down to how much unpredictability you can handle, and how long you’re willing to stay in the game.

A Little Side Note on Emotions

I’ve seen friends jump into small and mid-cap-heavy funds after seeing just one stellar year. “It gave 40% last year!” they’d say. And then boom, the market crashes, and they panic-sell at a loss.

The truth is, most people think they’re okay with risk. But when the numbers turn red, and your portfolio dips 10% or 15%, it can shake your confidence.

That’s why understanding your temperament is just as important as understanding the fund’s allocation.

Wait What About Taxes?

Let’s not forget Uncle Sam… or in our case, the Income Tax Department.

Both Flexi Cap and Multi Cap Funds fall under equity taxation rules. If you sell the fund units within a year, short-term capital gains are taxed at 15%. If you hold them for over a year, long-term capital gains above ₹1 lakh get taxed at 10%.

So taxes don’t influence the decision between the two. It’s more about how they perform and fit into your portfolio.

Long-Term Thinking Is Your Superpower

There’s something oddly comforting about time. Given enough of it, even the rockiest investments have a chance to grow.

Whether you go with Flexi Cap or Multi Cap, the real secret sauce is patience. Staying invested, not panicking during a dip, not chasing the next hot thing, that’s what separates successful investors from impulsive ones.

Both fund types are built for long-term goals such as retirement, a child’s education, or that dream house down the road. They’re not designed for quick wins or bragging rights at dinner parties.

One More Thing… Don’t Go All-In

Here’s a little tip that doesn’t get said enough: you don’t have to pick just one.

Why not invest in both?

Split your investment, say 60% in a Flexi Cap Fund and 40% in a Multi Cap Fund and see how they perform over time. Diversification isn’t just a buzzword. It’s a practical way to reduce regret.

If one underperforms one year, maybe the other balances it out. And if they both do well? Even better.

Final Thoughts From One Investor to Another

If you’ve made it this far, you’re serious about making the right choice. And that’s half the battle. Most people either jump in blind or stay frozen in analysis mode.

But here’s what I’ve learned from my investing journey: it’s not about picking the perfect fund. That doesn’t exist. It’s about picking something that matches your mindset, your comfort with risk, and your long-term vision.

So… Flexi Cap or Multi Cap?

Ask yourself: Do I want my fund manager to have the freedom to shift strategy as needed? Or do I like the idea of balanced, rule-bound exposure across all company sizes?

There’s no wrong answer, only the right one for you.

And hey, if you still feel unsure? That’s totally normal. Take a breath, start small, and just begin. The markets will always move. The real question is are you moving with purpose?

Post Comment

You must be logged in to post a comment.